BetaShares' Chief Economist, David Bassanese, recently held a webinar explaining why portfolio diversification is important and how this can be achieved through blending investment exposures to different asset classes. For those unfamiliar with BetaShares, they are a leading Australian fund manager providing a range of exchange traded funds, with over $6.5 billion in funds under management.

The key takeaway from this webinar is a story of asset allocation and how smarter asset allocation can lead to better risk-adjusted returns for investors.

Before looking at asset allocation, we need to first understand what is meant by an asset class. In general terms, they are a group of investments that have similar characteristics, expected to have similar risk and returns and to perform in a similar manner in a particular market condition. For example, we can think of the big 4 banks as being part of an asset class as Australian equities in the financial sector. More broadly, we can consider equities as a whole as an asset class, against cash, bonds, commodities etc. Each of these asset classes is expected to have a different risk/return profile and to perform differently under the same market conditions when compared with other asset classes. In statistical terms, we can expect that different asset classes will not be perfectly correlated.

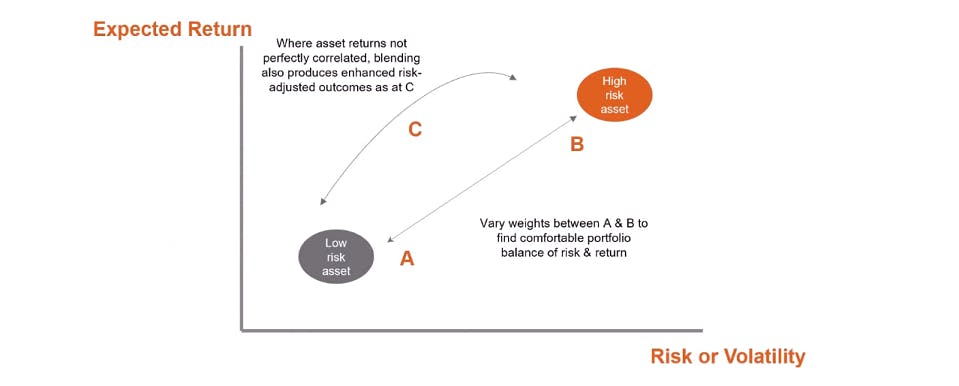

Where returns of investments are not perfectly correlated, this allows for the creation of portfolios combining different asset classes - providing higher levels of expected return for any given level of risk. This is visualised in the graph below, where there are two assets with different risk and return profiles, asset A and asset B. By varying the proportion invested in A and B, we are able to create a portfolio C, that provides higher levels of return than if A and B were perfectly correlated (the line between A and B). In essence, this is the theory behind diversification, and the age old adage "don't put all your eggs into one basket."

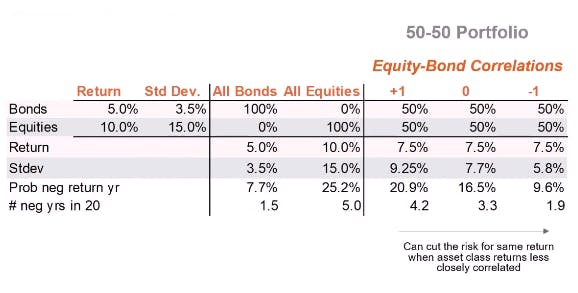

Looking at a hypothetical portfolio mixing bonds (lower risk, lower return) and equities (higher risk, higher return) shown in the table below, we can see that the benefits of diversification increase as the returns of the asset classes become more uncorrelated (correlation refers to the degree to which two securities move in relation to each other). The increased risk-adjusted returns are shown by the standard deviation, as a proxy for the risk of an asset, falling from 9.25% to 5.8% (from more risky to less risky) as asset class returns become less closely correlated (moving from +1, or perfect positive correlation, to -1, perfect negative correlation), with expected return stable at 7.5%. This means that by decreasing correlation through diversification, investors can achieve the same rate of return with lower risk.

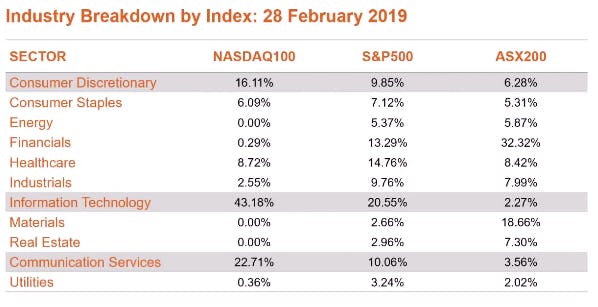

Diversification is a particularly pertinent consideration for Australian investors on the ASX. Looking at a breakdown of the ASX200 by industry, we can see that Financials makes up 32.32% of the market, with materials making up 18.66% and Information Technology a mere 2.27%. If we treat each industry sector as its own asset class with different risk and return characteristics, then it would appear that the Australian stock market has a very large exposure to financials and materials. The result is that investors, despite holding many individual stocks listed on the ASX, may have portfolios skewed towards certain industries and not taking full advantage of the benefits of diversification.

With a clear lack of Information Technology sector companies listed on the ASX, Australians have limited options to gain exposure to Australian companies in this space. Equitise is aiming to change this, by providing retail investors access to innovative Australian companies from a broad range of industries, from neobanks to craft breweries. As earlier-stage businesses than those listed on the ASX, the unlisted companies offered on Equitise can be thought of as a separate asset class to ASX listed businesses, with a risk/return profile that is more readily comparable to venture capital investments. Investment in these businesses can therefore form part of a broader asset allocation strategy, achieving higher risk-adjusted returns by creating blended portfolios (as seen in Portfolio C above).

In summary, David Bassanese explains that investors can achieve higher risk-adjusted returns through strategic asset allocation, with a portfolio spread across asset classes with lower levels of correlation being more effective. He elaborates by stating that many Australians investing in the ASX alone may not have exposure to a variety of industries in their portfolio due to the concentration of the ASX200 towards Financials and Materials. Investing in unlisted companies as an asset class can be a strategy to alleviate this lack of diversification, due to different risk/return profiles and different performance in similar market conditions.